He landed India's biggest carbon deal with a mockup website.

Now he's building the marketplace a $50 billion market never had.

If you’re new here, Welcome.

Welcome back to GVP. Every week we meet one Indian founder, verify the traction, and write the story so you can make faster investment decisions. We added 32 new subscribers last week — now at 529 investors reading weekly. If someone forwarded this to you, subscribe here.

This week we’re covering the following:

Why a $50 billion market still runs on phone calls and emails in 2026

How one founder landed India’s biggest carbon registry with a website that didn’t actually work

What carbon credits are, and why thousands of Indian companies are about to buy them for the first time

How HP ended up paying his engineers for free through a climate accelerator

Why the EU’s new carbon border rules make this relevant for global investors

What to watch for when evaluating early-stage climate infrastructure startups

“The best way to validate is when customers are willing to fund development or buy the product based on a vision or mock-up” - Atlanta ventures

Basil Paulose was studying sustainability at the University of Edinburgh when he stumbled into a problem that didn’t make sense to him.

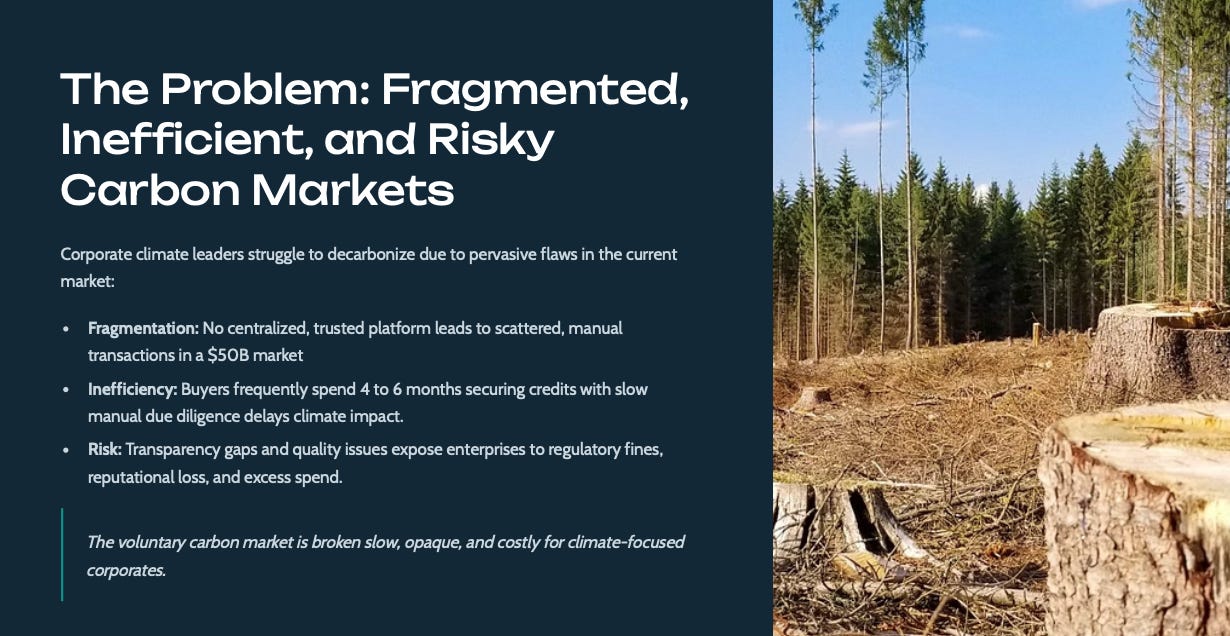

The carbon credit market, it is worth tens of billions of dollars and was still being run on phone calls, email chains, and broker relationships.

Buyers were spending four to six months trying to purchase credits.

The same carbon credit could cost $1 from one seller and $10 from another.

And nobody had built an infrastructure layer to fix it.

Not because the problem was invisible. Everyone in the market knew it was broken. But the people

building solutions were ESG consultants, not engineers.

The market didn’t need better policy. It needed someone who could write code.

So Basil quit his insurance job in London, flew back to India with barely any budget, and started building.

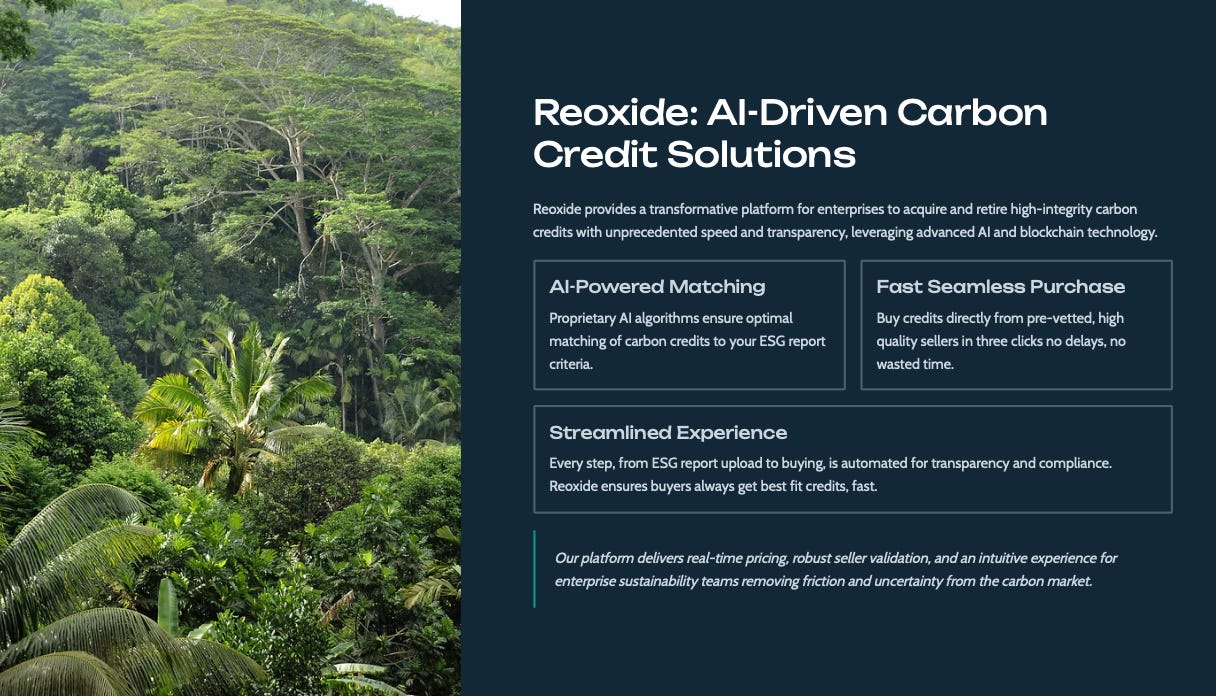

His startup is Reoxide.

He convinced India’s largest carbon registry to partner with him before the product existed.

This is the part that caught our attention.

Basil approached Universal Carbon Registry, the largest carbon credit registry in India with a framework website. Not a working product. Not a demo. A mockup.

The registry signed the deal anyway.

In Basil’s words: “We cracked Universal Carbon Registry with just a framework website. We didn’t even have the product. The market was so backwards that they were looking for new innovations.”

Then he had to actually deliver. Then Basil had to scramble, coding the actual platform himself with one

front-end developer, building custom APIs and webhooks to deliver on a promise he’d already made.

The market told him yes before he asked for money.

What are carbon credits, and why is this market still stuck in the 1990s?

For readers who don’t know about ESG, here’s the short version.

When a company pollutes like (textile manufacturer, an agriculture exporter, an apparel brand.. etc) they can buy carbon credits to offset their emissions.

One credit equals one ton of CO2 reduced or removed. Companies buy them to meet regulatory requirements or to position their products as carbon neutral.

The market for these credits is massive.

But it operates like a bazaar.

There’s no central marketplace. Buyers find sellers through brokers, emails, and phone calls.

A Nasdaq study found that 94% of carbon market participants still rely on phone and email to manage critical activities.

New credit listings take months to onboard. One in four market participants experience significant inefficiencies.

Price differences are extreme. The same credit might cost $1 from one seller and $10 from another, depending on how urgently the buyer needs it.

And there’s a trust problem on top of it all. Scams, double-counted credits, and weak verification have caused the voluntary carbon market to shrink by over 60% between 2022 and 2024.

Major companies like Nestlé and EasyJet have pulled back their credit purchases.

What Reoxide built, and how it works.

A corporate buyer uploads their ESG report to the platform. The AI parses the document, calculates the company’s emissions, and recommends a custom basket of verified carbon credits from pre-vetted sellers on the marketplace.

The platform is integrated with Universal Carbon Registry.

Sellers can list and delist freely — no escrow lockup, no fees to exit. Both buyers and sellers get a dashboard for tracking pricing, timing, and offset planning.

Reoxide takes 1% to 5% from the seller and 1% to 5% from the buyer on each transaction.

Future plans include subscription tiers at $20/month for basic reporting and $300/month for advanced features.

Why now: India’s carbon regulations are creating forced demand?

India has launched its Carbon Credit Trading Scheme. Core sectors are now required to report their emissions and offset them.

Indian exporters selling to the EU and Western markets also need to comply with those countries’ carbon regulations.

This creates buyers who have no choice. A textile exporter facing a regulatory deadline must buy credits.

They can’t opt out, and they can’t wait six months.

Basil is building specifically for these compliance-driven buyers.

Small to mid-size exporters in textiles and agriculture with 1 to 50 employees and revenues under half a million.

Companies that need to show carbon neutrality to keep exporting.

The go-to-market plan is phased. India first (already live with Universal Carbon Registry). EU next

(targeting biochar carbon credit sellers). Then Singapore.

The team behind Reoxide.

Basil Paulose (founder) — Master’s from the University of Edinburgh. Worked on a data project with the Scottish government. Then moved to London and worked in insurance before leaving to build Reoxide.

Dinesh (co-founder, CMO) — Currently at a fintech startup, Handles marketing and sales. Joined initially as an advisor and moved to a co-founder role in the last three to six months.

Three technical interns funded by HP through the Climate Collective accelerator, one of the largest climate accelerators in Southeast Asia. HP pays their salaries through a sustainability grant. No equity was given. The interns work with Reoxide for three months.

Reoxide has also been through Draper’s founder program.

GVP’s take

Why did we pick this one?

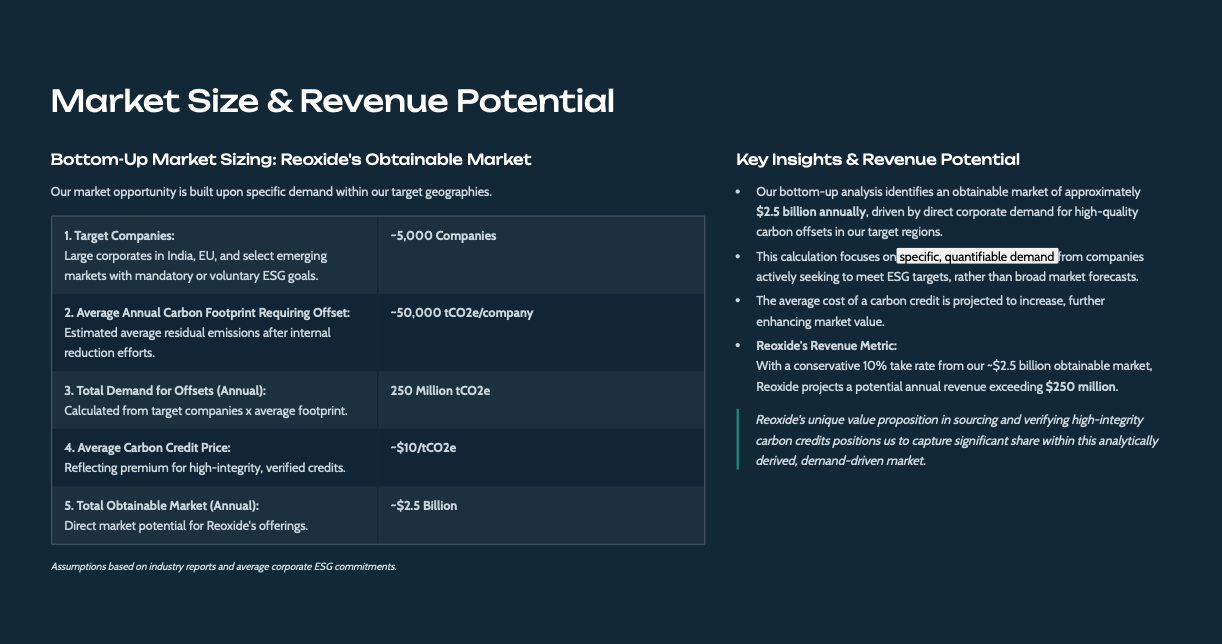

India made carbon credits mandatory for around 490 companies in April 2025. The first actual trading hasn’t even started yet — that’s expected mid-2026. So the market is being built right now. Almost nobody is in it.

And there’s another layer. The EU just started pushing Indian exporters to prove their carbon footprint. If you’re a textile company or an agriculture exporter selling to Europe, carbon credits aren’t optional anymore. They’re part of the trade paperwork.

He closed his first partnership before he had a product. That tells you something about the founder. When the biggest registry in your country signs a deal based on a mockup website, it means the market is desperate for what you’re trying to build.

HP is paying three of his engineers through a climate accelerator grant. No equity given. No cash spent.

For a pre-revenue startup, that’s smart resource management.

And the core gap is real. A multi-billion dollar market where 94% of participants still rely on phone and email. That’s an infrastructure problem waiting for a technical founder.

P.S. One last thing…

If this was useful, forwarding it to one person in your network is the single best way to support what we’re building.

500+ investors already read this every week, including firms like Accel, WTFund, and Ice VC, alongside family offices from Dubai, Singapore, and Europe.

Our only promise is this: we will keep finding India’s best founders at the earliest stage, so you never miss a deal worth taking.

See you next week

If you want me to make a warm intro with this startup founder, feel free to reply to this email!

Email: jaylee@globalventureplay.com

Such an under researched article, I even dropped a message to Basil on this. It gets some fundamental aspects of carbon markets materially wrong, which can mislead readers and investors.

The biggest issue is the conflation of voluntary carbon markets with compliance systems. India’s Carbon Credit Trading Scheme is not a blanket requirement for companies to “offset” emissions. It is an intensity-based compliance mechanism for a defined set of obligated entities. Presenting it as broad, forced demand for carbon credits is simply incorrect.

Similarly, the linkage to EU regulations is misrepresented. Mechanisms like CBAM do not require companies to buy carbon credits to keep exporting. They require emissions reporting and payment for embedded carbon. These are very different instruments, and conflating them creates a false demand narrative.

The statement that “carbon credits became mandatory for ~490 companies” is also inaccurate. What is mandatory are compliance targets under a regulated framework, not participation in an open carbon credit market as implied here.

The buyer profile described (small exporters with 1–50 employees) does not align with how either compliance or voluntary markets function today. Compliance demand is concentrated among notified, emission-intensive entities, not SMEs in general.

There are also unsubstantiated claims such as “largest carbon registry in India” and broad market sizing statements that need clearer grounding.

The infrastructure gap highlighted is real, and the opportunity for better market rails exists. But the current framing overstates regulatory demand, misrepresents policy mechanisms, and blurs critical distinctions between market segments. That makes the overall thesis directionally interesting, but factually weak, inaccurate and very false.

Bad story.