She paid herself in feedback, not cash

That's how a solo founder got her first two clients in India's $5B compliance market

📌 Aisha is one of the founders selected for the Women in FinTech program at India’s GIFT City. Keep an eye on these Indian women fintech founders. What they’re building deserves your attention.

Also, special thanks to Sweta Tiwari and Plug and Play APAC for connecting us with the founder.

If you’re new here, Welcome.

Welcome back to GVP. Every week we meet one Indian founder, verify the traction, and write the story so you can make faster investment decisions. We added 32 new subscribers last week — now at 634 investors reading weekly. If someone forwarded this to you, subscribe here.

My dear fellow investors,

She identified this problem fresh out of college.

Fresh out of college, Aisha Peenwal walked into her first job at a fintech company in Chennai.

On her first week, a new RBI circular landed. A dense, 40-something pages, full of legal references to documents from years ago.

Her manager told her to figure out what it meant for their product.

It was a major regulation, the kind that touched almost every partnership and product running in Indian fintech at the time.

She went to four senior colleagues. She got four different answers.

Nobody was sure. Everyone was guessing. And somewhere in that room, a small process gap was turning into a compliance risk.

She filed it away in the back of her mind and got on with her career.

What made her believe this was finally solvable?

Aisha spent six and a half years in fintech product management, working on loan origination systems, working capital engines, and business rule management at companies including Credable.

In 2024, she saw a large NBFC get fined 50 lakh rupees and decided the problem was now solvable with AI.

She had taught herself Python over five years of weekends, calling friends at odd hours when she got stuck on a syntax error, staying up until something worked.

She built the first version of ReQL herself.

Her first client didn’t pay her in money. She asked them to pay her in feedback.

Two hours, sometimes three, sitting with the CEO of a small NBFC, mapping out every compliance use case the company faced from the inside.

Why is this problem getting worse, not better?

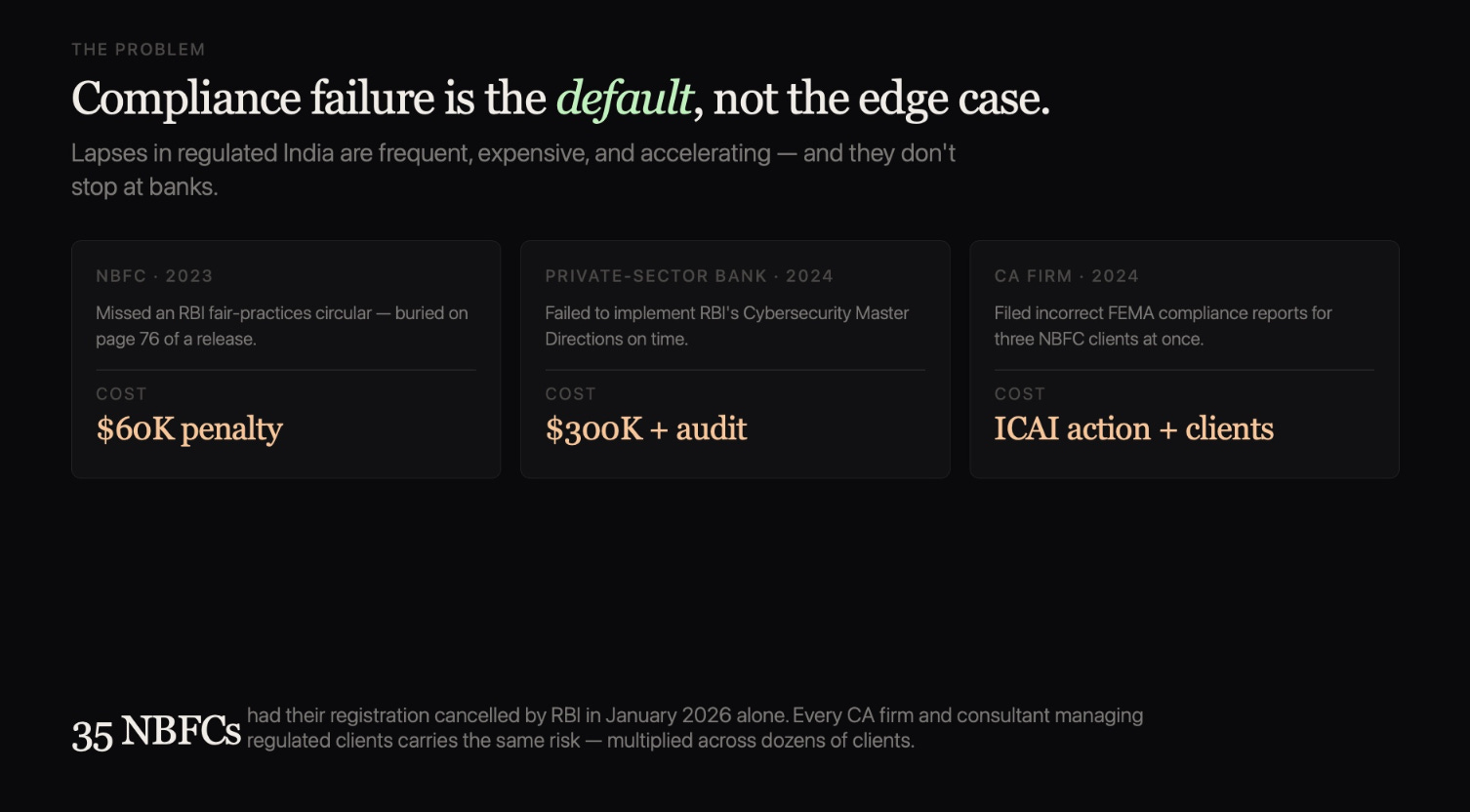

India has 9,000 registered NBFCs, 140 scheduled commercial banks, 57 insurers, and over 70,000 CA firms advising regulated clients.

Together they face over 1,200 new regulatory circulars every year across RBI, SEBI, IRDAI, MCA, PFRDA, and other regulatory bodies in India.

That’s roughly 80 updates a day.

Every entity reads those circulars separately. Every entity draws its own conclusions. Every entity hopes it got it right.

In December 2025, India’s central bank shut down 35 finance companies all at once.

The reason: these companies had been breaking small rules for months, and nobody caught it in time.

Nobody is breaking these rules on purpose. They are struggling to keep up with the updates.

How is ReQL solving this big issue?

ReQL is a small language model trained on India’s regulatory corpus.

Tell it what kind of entity you are, and it maps every obligation that applies to you across every regulator.

When a new circular arrives, it tells you what changed, what it means for your specific business, and what you need to do next.

Every answer comes with a citation — the exact circular, clause, and obligation — so you can show a regulator the proof, not just the intention.

The platform covers 28 use cases today. It is deployed with two NBFCs. Aisha is in active conversation with one of India’s three largest private banks, a connection she made through the Plug and Play cohort at GIFT City.

What do we like, and why are we featuring this startup?

The founder has six and a half years of insider knowledge of exactly the problem she’s solving.

She built the POC herself. Her first two deployments came from personal relationships, which means she can sell.

The enforcement data is moving in her direction 35 NBFCs lost licenses in one month, and that number is only going up.

India’s RegTech market is projected to grow from roughly $600 million today to over $5 billion by the early 2030s.

That growth is being pulled by 9,000 NBFCs, 140 banks, and 70,000 CA firms who all face the same problem and currently have no shared solution.

What we’re watching: this is pre-revenue. The enterprise sales cycle in Indian banking is long.

The private bank conversation is promising but not closed. The real proof of concept is the first paid client.

P.S. One last thing…

GVP has 634+ investor subscribers — including partners at Accel, principals at family offices in Singapore and Dubai, and angels across the US, Australia, and Europe.

If you forward this newsletter to 3 investors who subscribe, we’ll make a warm intro for you to any family office or VC in our network you’d like to meet.

See you next week

If you want me to make a warm intro with this startup founder, feel free to reply to this email!

Email: jaylee@globalventureplay.com